![]()

July 2021 Newsletter

Submitted by Dorval & Chorne on July 1st, 2021

Keagan Kinsella | July 1, 2021

Keagan Kinsella | July 1, 2021

My oh my, it’s July and we are halfway through 2021! I guess time flies when we’re in a post-pandemic “normal world”!? In this month’s newsletter we’ll be talking about:

- This crazy hot real estate market- tips to put you in the best home buying place as possible, and my sister’s home buying experience!

- Do you prefer your gas cheap or expensive?… How about your investments?

- Question of the week: “Am I diversified? And what does that even mean?”

The wild, wild, real estate market

Here’s a fun fact for you (well, fun if you’re selling a house…not so much if you’re buying). For the first time ever, over half of homes sold in the US went for above asking price in May, according to Redfin. In fact, the average sale was 2.2% above what it was listed for (which for a $500k house is $11k!).

If you’ve been in the market, or heard anyone talk about the process, you likely know what a challenge it is. My sister is one of those people! She bought a house in April of this year, after months of showings, unaccepted offers, and letdowns. She was looking in the St. Louis Park (MN) area, which being a hotspot location meant things were expensive and going fast!

One of the things she did after months of missing out on houses, was look for the houses that have been on the market longer, and see if there was anything she could get that isn’t going to sell for $30k above ask price. Her realtor suggested they switch their strategy from looking at the new listings just posted to digging deeper into the houses that had been on the market for longer, and figuring out why.

This led them to go check out a place that had been listed for almost a month and a half. The home was in a prime location. It actually had been dropped in price too. The kicker was it was halfway flipped! The seller started the process, but then was not able to finish. This meant it had some really nice perks (new paint, fixtures, appliances) …but needed some help in other places (basement, kitchen cabinets, flooring). Since she wasn’t competing with 20 other offers, she was able to come in below asking price, and negotiate. She didn’t have to waive an inspection either!

The reason I am writing this is because from a financial planning perspective, if you are willing to put in some time—there are a lot of homes out there that with a little love, (and $$$!), could be the perfect place.

Personally, I would rather put the money into renovations to improve the house vs. paying thousands of dollars above ask price. But, it all comes down to quality of life though! If you find the perfect place, and you’ll pay whatever you need to do get in it, it doesn’t matter what anyone else would do, because that is what is important to YOU! Housing is one of the most important decisions from that perspective because it is where you spend a lot of time.

Here is a before shot of her kitchen, and a photo of where it is now. My parents and aunt were able to help her put in the sweat equity to make quite the transformation… and it’s not even finished yet!

I like to buy my gas cheap, but stocks cheaper!

Does anyone else remember when gas was less than $2 per gallon?! You probably do, because it was only about a year ago! The U.S. average price for a gallon of gasoline has been on a steady incline since things bottomed out in April of 2020, and now the average cost per gallon in the US is $3.09.

In April of 2020 you could also get a share of Nokia (a meme stock which you may recognize if you paid any attention to the whole GameStop, AMC short squeeze) for the cost of a gallon of gas! In January, when the Reddit traders were manipulating the market, the price of Nokia skyrocketed to nearly $6/share… and it was celebrated! When gas prices skyrocket up…why don’t we celebrate?

This is a small example, and I know gas is not an investment, but it illustrates an even bigger concept we see all the time in the financial planning world. Stocks and bonds are neither good nor bad… they are simply tools! When stocks (or stock mutual funds) go up in price, it means the underlying companies are more expensive. However, when someone sees a stock that is up a lot, they often want to buy that stock because they think it is better. Would you rather buy a share of Amazon stock at $2,000 or $4,000? The share of stock is simply more expensive at $4,000… when in reality it is the same company!

So, keep this in mind when the stock market declines, and you see your 401k or investment accounts take a dip. That doesn’t mean you need to get rid of what you have because it is down, and “bad.” It’s simply cheaper! In that situation, you are following the advice of the old adage, “Buy low, sell high!”

Question of the week: “So…Am I diversified?”

It’s a common trend for people to come in to talk to us because they’ve been told “they should or shouldn’t be doing something” but they aren’t sure what that something that they are doing means! We met with someone last week who came to us asking if they were diversified in their 401k because they only had one fund. Everything they had heard told them “Don’t put all your eggs in one basket!” But when we got down to the root of the question, they didn’t know what diversification really meant!

This is a common question we get especially because in many employer sponsored plans, the default option is a target date fund. If you are wondering what a target date fund is, it’s basically a “set it and forget it option” where the fund is managed according to retirement date selected. It will automatically get more conservative (less stocks, more bonds) as you get closer to retirement.

It is what is called a mutual fund. A mutual fund by definition is an investment that trades diversified holdings and is professionally managed. When you hear “diversified holdings,” this means you own a variety of different stocks and bonds inside, but it is packed up into a fund.

Lots of people ask us if they should be buying Amazon, or Google stock because they hear their friends talking about how much money they are making in their Robinhood account (they literally feel financial FOMO). We always let them know, you actually do have those stocks, but just in little bits and pieces! The benefit of having little bits and pieces means you aren’t subject to the volatility of having all of your money in that one stock.

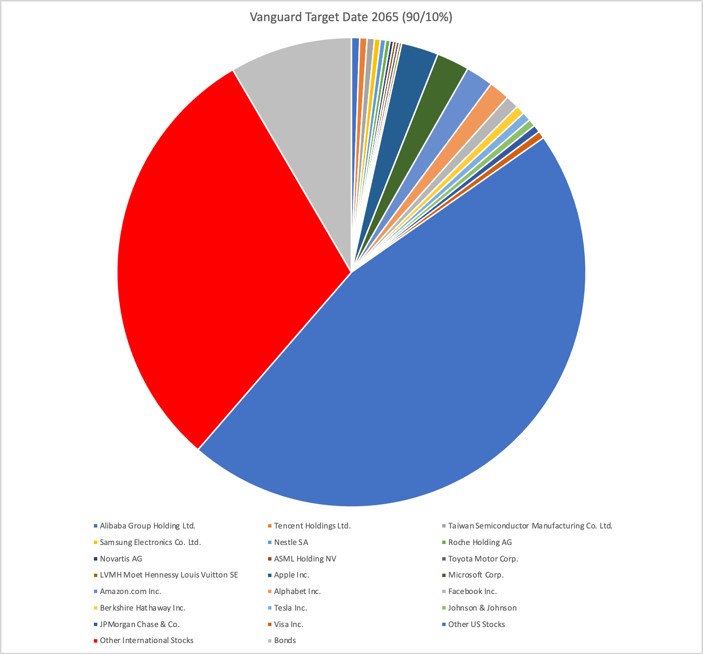

After that question was asked to us, I was personally curious as to what the true breakdown of a target date fund for the year 2050 (meaning for a young person who doesn’t plan to retire for about 30 years!) This pie chart might look a little overwhelming, but I am here to break it down for you.

In the top right hand side of the pie, you see slices of large, well-known companies such as Amazon, Apple, Alphabet (Google), and Alibaba… to name a few. Like I mentioned before, this is a little bitty piece of the pie! But these holdings are actually significant enough in size to not be grouped into the big red, blue, or gray chunks of the pie.

Blue= Other US Stocks

Red= Other international Stocks

Gray= Bonds

To me, this is a great illustration to show that although you may log into your account and see one fund—you actually have much more than what meets the eye! It is also constantly changing and the percent “pie slices” are going to evolve based on what the market does. In this kind of fund, the beauty is… you don’t have to worry about it! No need to have financial FOMO.

All right, that’s it for this month! In July I’ll be getting married and headed out on a honeymoon, so stay tuned for my next newsletter in September where I will continue to share and inform in new and creative ways. If you want to sign up for the newsletter email, click here (and let others know they can sign up.) Last but not least, let’s connect on LinkedIn!

Advisory services provided through AdvisorNet Wealth Management (AWM) and Dorval & Chorne Financial Advisors. Dorval & Chorne Financial Advisors and AWM are not affiliated.